IS YOUR HDB AN ASSET

This is the most common question in the head of all HDB owners. Is my HDB worth anything in the future? Is my HDB an asset for future earnings? We all like to treat our HDB as a asset. But unfortunately, HDB has an expiry date, HDB are all based on 99 years lease.

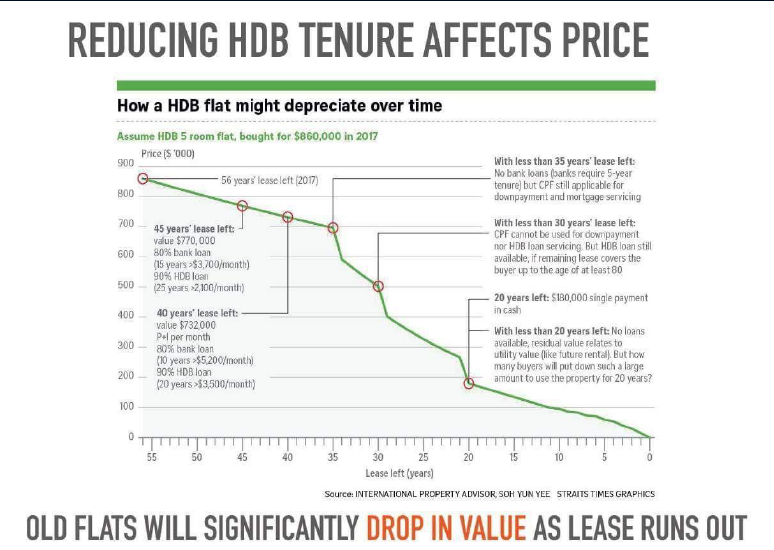

And as the HDB becomes older, the remaining years till 99, will become lesser.

Your HDB value will get worse each year as the 99-year leasehold shortens. And the longer you stay in your HDB , the remaining value will diminish. To make things worse, when the remaining leasehold of your HDB is fewer than 60 years, it becomes harder to sell. Because CPF usage is restricted further and bank loans are tightened for purchasers buying properties will less than 60years of Lease remaining.

And with restrictions on PR to stay in Singapore for 3 years before they can qualify to buy a HDB, this will dampen the demand for resale properties too.

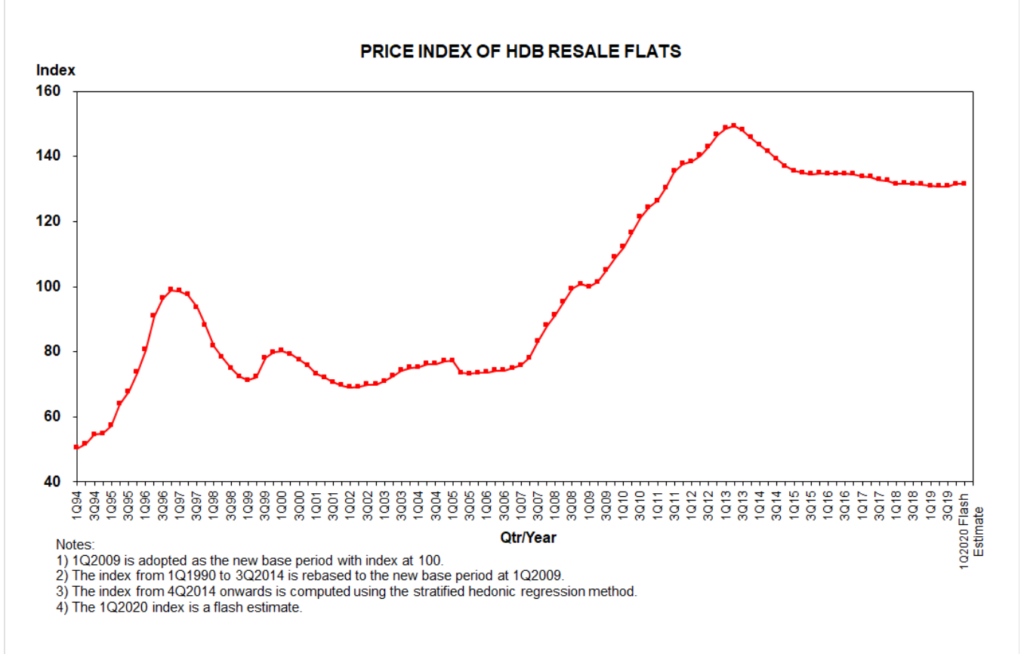

According to the HDB resale price index, we have seen a decline in HDB resale prices since 2014.

HDB RESALE PRICE INDEX

Based on the latest HDB flash report, the Housing Board resale prices were flat in the first three months of 2020, as compared with the last quarter of 2019.

The resale prices for 1st quarter was flat, 131.5 after two consecutive quarters of increase in 2019, with 4th quarter reported 131.4 and 3rd quarter reported 130.9.

The HDB has offered many new BTO flats last year, 4571 units in Nov 2019 and 3373 units in September 2019.

And in upcoming May, HDB will offer about 3,700 Build-To-Order (BTO) flats in Choa Chu Kang, Pasir Ris, Tampines and Tengah.

In August 2020, HDB will offer another 4,100 BTO flats in matured towns Ang Mo Kio, Bishan, Geylang, Tampines and non matured town Woodlands.

With so many BTOs, buyers will have many choices to select and may not look for resale HDB, thus may cause a drop in demand for HDB resale.

With all these in mind, it is not good to treat your HDB as an asset or an investment.

For it to become an investment , the HDB property must be

- Able to generate positive cashflow, or pay us money in form of rentals

- Able to generate Capital Appreciation or growth in value when we resell the unit

- Provides us leverage for value, eg. Mortgage equity

Generally, many have used properties as a financial asset to hedge against inflation and to track growth in the country. When a county performs well economically, usually the properties prices will move along with it.

Many fast developing nations, like HK, S Korea, and Singapore have benefited from this growth. But moving forward, future growth is not so fast, and we cannot expect such growth rates as before and hence we will not see similar price gains in properties.

Hence it is no longer possible to buy a resale HDB and expect a sizeable profit in the near future.

Recently, there has been a lot of noise about HDB flat reverting to zero value and return to government at the end of their 99 year lease.

Based on theory, it is true the HDB units will revert back to HDB when their lease expires. We are still waiting for official reply from the government , will there be a lease renewal policy or will it offer rehousing policy to those whose units expires. This uncertainty has to be resolved by government to put the HDB buyers at ease.

And there are a growing number of old HDB flats with mounting depreciating values, where owners are holding to properties which are near the halfway mark of their 99 year lease.

The long held ideology that HDB is not just homes but appreciating assets was implanted in us during the campaign of asset building with HDB by the Government.

But today this is not true, old HDB flats are driving many to think otherwise.

Although HDB is a necessary asset, because we need a place to stay. If we don’t buy a HDB we have to rent a place and either way, it is money spent, so it may as well be spent on your own HDB.

So, all homebuyers has to view HDB as homes and not as investments.

Because of this viewpoint, the Government will not allow ageing flats to be ignored. The government is committed to maintain and upkeep all HDB regardless of age through HIP or MUP programs. The Government will not allow general degradation of HDB.

As such the Government has recently introduce some measures to encourage buyers to buy old HDB properties.

Included in this measure are new enhanced housing grants (grants up to $80,000) for first time buyers and raising income ceiling for all eligible HDB buyers (new cap $14,000).

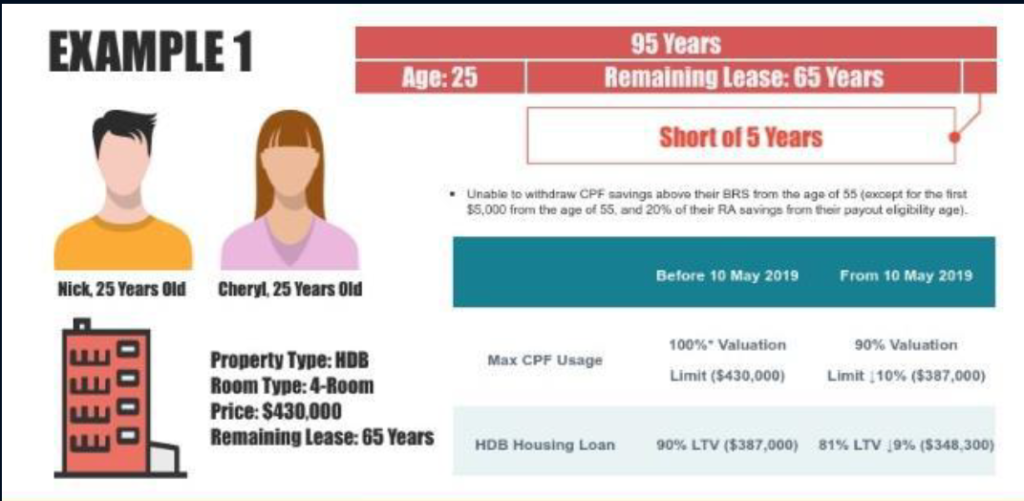

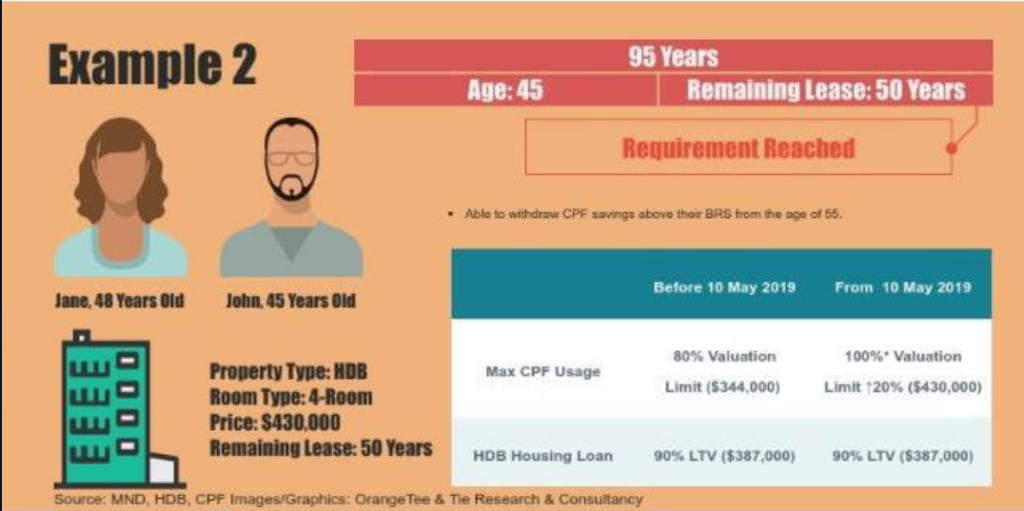

Starting from May 2019, Home buyers can draw more from their Central Provident Ordinary accounts to buy old HDB flats, provided the property’s remaining lease covers the youngest buyer till the age of 95.

HDB buyers will also be entitled to Housing Board loan of 90 per cent (maximum loan) of the property price and max CPF usage of 100% valuation.

This new move by the Government is a new shift to focus on whether the property can be a home to the owner for life, instead of focus on its remaining lease. This move will ensure that the HDB home buyer will have a roof over their heads in their old age.

Because old HDB property flat price depreciates over time, it is advisable to get one with more remaining years, because when add to your age, it must be able to cover the youngest buyer till 95 years.

Buying an old HDB flat with the view that it will fall into SERS is not correct thinking. Because there is no guarantee that SERS is happening to all old properties. Our Singapore minister has already said that SERS, Selective EnBloc Redevelopment Scheme, is not a guarantee issue. In fact only 4% of all HDB built are selected for SERS , said Mr Lawrence Wong, Minister for National Development.

With all these in mind, HDB may not be an investment or an asset.

Because an asset is one that will put money into your bank, it will generate income for you.

PROPERTY WEALTH PLANNING

So, it is best to consider Property Wealth Planning (PWP) strategies to maximise and deploy their funds to work for them. So what is PWP and how does it work ? It is basically unlocking your dormant capital and convert it into active capital or income generating capital.

One way is to sell your existing HDB and use the sales proceeds to buy 2 condo, one for own stay and another for rental investment. It can be from new launch condo sale or from resale condo.

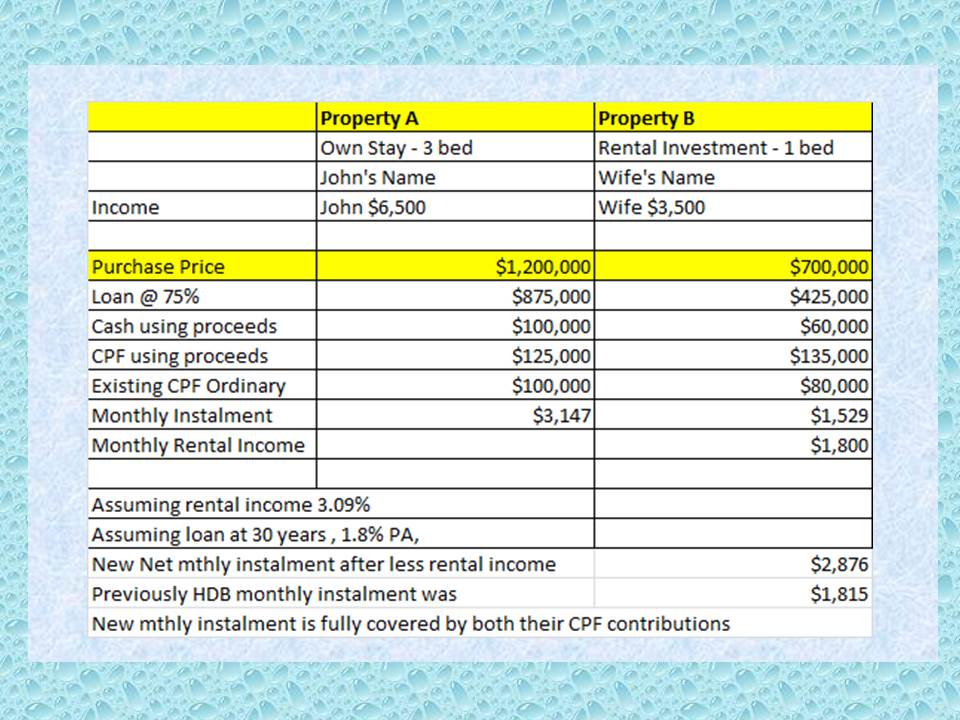

Example : If John Teo (35yrs) and his wife (32 yrs) has a HDB 5 room

He could sell it

House value at $620,000

Outstanding loan $200,000

Sales Proceeds : $620k – $200k = $420,000

Assuming return CPF $260,000

Net Cash $160,000

Current HDB instalment $1,815 per month (Borrow $400,000 @ 2.6% over 25 yrs)

John allocates his sales proceeds money into 2 properties.

His monthly instalments is easily covered with his rental income and his CPF contributions

It is a very good time now to sell the property despite the COVID 19 situation.

Property prices have been gradually increasing month on month.

New home sales has been doing very well since beginning of year. In Jan, there were 618 units sale and in Feb 2020, new home sales jump 57.3% or 975 units.

Even IMF has reported that they expect a sharp rebound to follow after the corona virus pandemic.

CONCLUSION:

HDB is not really an asset to make money, although there may be capital gain if you have bought your HDB more than 10 years ago.

HDB is merely for home stay. But it can be monetized after 5 years MOP.

You can then use the sales proceeds to buy condo for your own stay.

When you sell your HDB, you are required to return to CPF, the accrued interest for the amount that was withdrawn for housing. So if you decide to delay in selling your HDB, means you stay longer and you incur more accrued interest.

With reduced appreciation of HDB and the increasing accrued interest, it would mean you will receive less cash proceeds upon selling.

Hence it will be a good time to convert your HDB asset into a real income asset. With good Property Wealth Planning, you could be a owner of 2 new condos, do call me , Rick at 9109 2177 for a discussion.

Schedule time with me

Article by Rick Fok

Rick Fok is a realtor with OrangeTee & Tie Pte Ltd. He has been in this real estate business for 9 years. He is very focus in helping his clients rent properties and he does help many customers to buy new projects according to their needs. His interest include sports such as running and soccer besides just real estate work. He loves to connect with people to discuss properties related issues and gets enormous satisfaction in helping them fulfill their needs. If you have any queries on this topic or other , please do give Rick a call and we can discuss this over a cup of coffee.

Other Articles to read

Is it better to buy an EC than a condo ?

Buying a new launch or a resale property. Which is a better property for investment?

Do you keep or sell your HDB , when you upgrade to a condominium.