SELL HDB AND BUY TWO CONDO. HOW IS THIS POSSIBLE ?

It is the common goal of many HDB owners to upgrade to condominium. Their main reasoning is that condo comes with facilities and they can enjoy and upgrade their lifestyle. When approached by client to do this, I will first check on their financial feasibility and sometimes may even advise them to sell HDB and buy 2 condo instead.

How does sell HDB and buy 2 condo work ? Well, it is to sell your HDB and use the proceeds for down payments for 2 new condos. Under this “sell one & buy two” strategy, the seller is urged to sell the HDB to capitalize on capital appreciation and use proceeds to buy 2 condo units (1 big and 1 small condo).

The name of one spouse is used for the big condo for family occupation and the other spouse name is used for the smaller investment property which is to be rented out.

Sell HDB to buy 2 new condos

By using the 2 individual names to buy 2 condos, we have avoided the issue of ABSD for the second property. By the power of leverage, we can sell one property and borrow enough money to buy two condos. This 2 purchases are done by using a combination of cash and CPF monies.

Assuming the mortgage on the investment property is partially funded by CPF monies, while the rental income covers the balance, there is the possibility of positive cash flow. This will give passive income to the seller.

By adopting this strategy to sell HDB and buy 2 condos, you will gain the following.

1. You save thousands for not paying ABSD

If you buy a new launch condo and keep your existing HDB, or buy 2 condos with both names you have to pay 12% Additional Buyer Stamp Duty (ABSD). Eg. If you buy a $1 million investment property you have to pay $120,000 tax.

That is equal to 4 years or 48 months of rental income if you will to rent HDB out for $2500. It is better to use this money to pay as downpayment for your 2nd condo under a different name.

2. It works against Inflation

Real Estate is the best choice against inflation. It is not just the increase of the resale value of the property over time, but the property can be used to generate rental income.

However, if you own only HDB flat, it is merely for own stay, but not used to hedge against inflation. While if you buy 2, you can have one for own stay and another for rental income.

3. HDB Flat is Aging, and lose value

It is good to sell HDB especially if the property is already old. Because for the purchase of any residential property less than 60 years remaining lease, the maximum amount of CPF that can be used is capped at a percentage.

You cannot use their CPF fully, you will need to pay part of it by cash. That’s why those older flats couldn’t fetch a good price despite having a superb location and even well maintained.

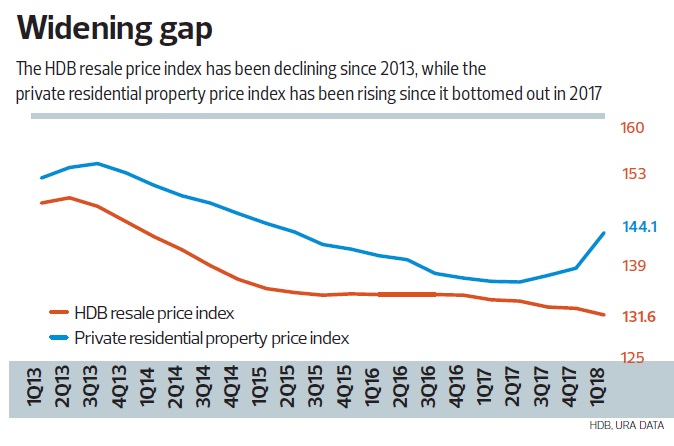

4. Widening gap in price index: HDB vs Private properties

Private property index has gone up sharply in recent quarters but the HDB resale index has continued downwards.

With condo price going higher and HDB price going lower, it is good time to sell HDB and buy condo. This will give you more future value to your new condo acquisition.

5. Flexibility to swap between your 2 Condo based on Your Own Needs. Enjoy the Condo Facilities and Lifestyle

You see, when you own 2 properties, you can stay one and rent out one. You have to stay in the bigger one while your children are still young. So you choose to stay in the 3 bedders and rent out the 1 bedder.

But when your children grow up and form their own family in the future, you will have 2 vacant bedrooms. That’s the time you may consider to move to the 1 bedder and rent out the 3 bedders. This will be when you can really retire comfortably.

Before we embark on this strategy we must understand the concept of it.

Concept 1: Understand the amount of monies entering your CPF accounts

If you are working on a monthly salary, you will receive CPF contributions from 2 areas:

- 20% from employee (you)

- 17% from employer

These monies are then split and put into your:

- Ordinary Account

- Special Account

- Medisave Account

How it is split will be dependent on your age .

These monies are sitting quietly in your CPF accounts, earning the 2.5% interest in your CPF Ordinary Account, subject to CPF Board’s terms and conditions.

Is it a better way to utilize these CPF monies and invest in properties where they can work harder to earn returns

Concept #2: “Freeing up” the CPF monies to channel into your 2 new properties

The concept of selling your HDB flat will free up more CPF monies for you to channel into your 2 new properties.

It is interesting that people often forget how much money they have paid into their HDB flat since they first bought it. It could be a substantial amount, maybe hundreds of thousands.

Especially if your flats have appreciated in value, it will “free up and unlock” more funds than what you originally put in.

For those flats that didn’t appreciate, it may result in a negative sale where you might not be able to get any money from a sale.

That is why you need to get expert advice on a detailed financial calculation

Concept #3: HDB Flat Valuation

The HDB flat valuation is important as it determines the selling price and eventual cash proceeds. This is usually done by buyer of HDB flat to get HDB loan.

The value of the flat can be estimated from similar transactions that has occurred within the same block or nearby vicinity.

With this valuation, you will be able to get enough cash proceeds to buy 2 properties

- Amount of CPF monies available from husband and wife

- Amount of investable liquid cash available

If all is well, you should have more than enough to proceed to purchase 2 properties under 2 different people’s name.

Property A will be under the husband’s name.

Property B will be under the wife’s name.

One of the properties will be the matrimonial home while the other is rented out for passive income.

How does “sell one buy two” work?

It mainly works through the power of leverage. To be more precise, it means you need to “sell one and borrow enough money to buy two”.

Disadvantages of this scheme

With job security at stake amid slowing economy, MAS warns of risks involved.

- Amid a slowing global economy, being laid off is a possibility and the property’s value depreciating are real possibilities. Both these scenarios will cripple the couple’s ability to service two mortgages at the same time. Property purchases are significant and long-term commitments, the investor or buyer need to be aware of the risks involved.

- In order for this strategy to work, both buyers must continue to work to have sufficient income to service their individual property loans. Should one spouse lose their job, it could place strain on the family to service two mortgages at the same time.

- In any property purchase, there is a need for substantial upfront cash, the buyer has to consider whether they have sufficient savings to pay for all the relevant stamp duties and cash down payments before making property purchases.”

Another potential issue as pointed out by Propnex’s Mr Ismail, is that “Property investments are illiquid. You can’t cash out tomorrow. In the event of a downturn, you may not be able to find a tenant.”

That is very true, you cannot cash out immediately, and because of uncertainties in the global economy you may not be able to find a tenant to help pay the mortgage of your investment property.

So it is best that buyers do not plough all their savings or cash reserves into the investment property purchase, but instead do maintain cash reserves amounting to at least one year’s worth of mortgage instalments as a safety buffer.

By selling your HDB and buying 2 condos, you have to remember that condo purchase do include the following

With economic uncertainties, bank interest rates fluctuate, so make sure you can service the loan when they go up.

Unlike an HDB loan, bank loan rates fluctuate. They’re now hovering around two per cent per annum, but historically, the average is around four per cent. And since they’ve been at historical lows for around a decade, there’s little room to move except to go up

2. Two people sharing a mortgage is a much smaller burden than each one taking on their own loan.

When you buy 2 properties with the cash proceeds from selling your HDB, you have to take 2 loans for buying 2 new properties.

The sum of these 2 loan mortgage quantum can be quite high and may take out huge chunk of your family combine income..

For Hubby – Buy a 3 Bedroom condo for own stay

- Assume purchase at $1,500,000. At 2 % per annum, a mortgage loan 75% is $1,125,000

- Assume loan tenure of 25 years, mortgage is about $4,763 per month.

For Wife – Buy investment shoebox unit for rental

- Assume purchase at $800,000, At 2% per annum, mortgage loan 75% is $600,000

- Assume loan tenure of 25 years, mortgage is about $2,540 per month.

You must be prepared to pay $2,500 plus maintenance fees (est $300 ) whenever your unit is untenanted.

Conclusion

Is the concept of selling your HDB to buy 2 condos a good idea?

In short, “sell one buy two” can work, but only for those who have done very well for themselves since the time they first bought their flat (or maybe they sold their flat for a million dollars).

With private property prices increasing at a faster rate than wage growth, property experts are saying that the affordability gap for private homes could further widen for Singaporeans.

While median asking prices of private property have risen by 12 per cent in the last three years, monthly wages have increased only by 7 to 8 per cent over that period based on Ministry of Manpower figures.

Hence it may be a good idea to capitalise on selling your HDB and buying into private properties when you can afford. Perhaps, you should take this route of “Sell HDB to buy 2 private properties” only if you have a really comfortable budget for mortgage and at least 20 year investment horizon.

Though the strategy is not a new one, many buyers are now keen to go for this strategy or to find out more about it given the double-digit ABSD if you buy a second property. I must say again that this strategy is not for everyone. “You have to be financially stable. Both (spouses) have to have fairly high income,” to service the loans, and it must be done with a perspective that property ownership is for the long-term.

Schedule time with me

Article by Rick Fok

Rick Fok is a realtor with OrangeTee & Tie Pte Ltd. He has been in this real estate business for 9 years. He is very focus in helping his clients rent properties and he does help many customers to buy new projects according to their needs. His interest include sports such as running and soccer besides just real estate work. He loves to connect with people to discuss properties related issues and gets enormous satisfaction in helping them fulfill their needs. If you have any queries on this topic or other , please do give Rick a call and we can discuss this over a cup of coffee.

Other Articles to read

Is it better to buy an EC than a condo ?

Buying a new launch or a resale property. Which is a better property for investment?

Do you keep or sell your HDB , when you upgrade to a condominium.