Do you keep or sell your HDB , when you upgrade to a condominium.

Many of the Singaporeans will start out with buying a HDB flat as their first home property.

And when they upgrade to a private condominium in the future, they are faced with this impending question, to keep or to sell their first matrimonial home.

Before anyone can answer this, we have to look at how it work out financially for the couple and reasons to why they intend to keep the property.

What is your objective in buying this second property, is it to earn rental income from either the HDB or the condo. If it is for investment, will the rental income be able to service the mortgage loan? Will it have a drastic impact on your finance, if you are unable to find a tenant.

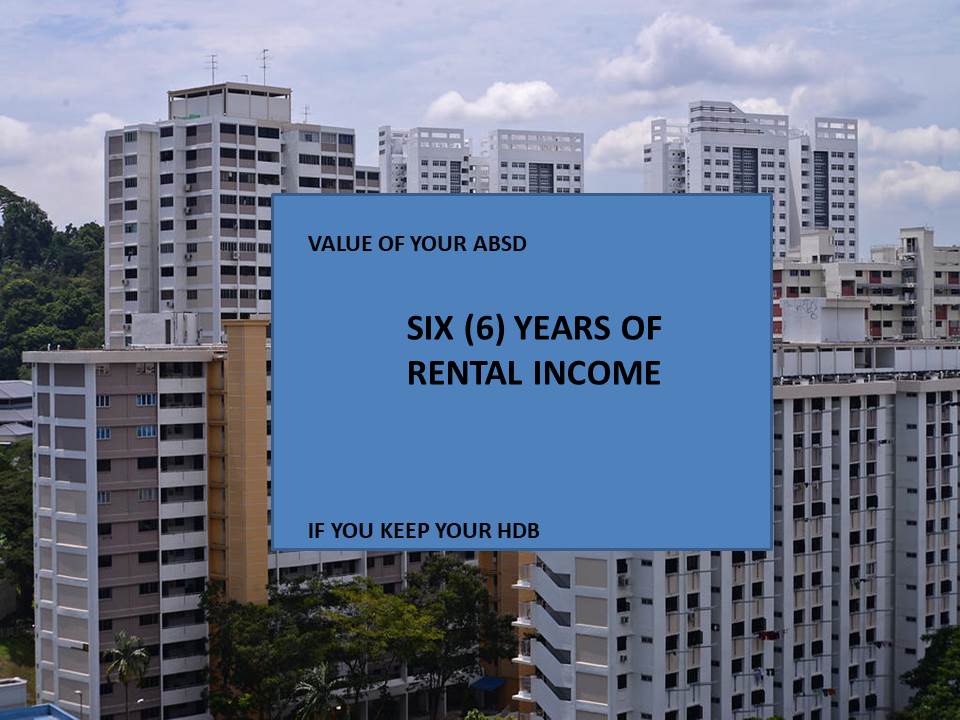

If you intend to rent out the HDB and move into the condo, the important factor to consider is to consider the potential income versus the additional expenditure incurred (ABSD).

Eg. To rent out existing HDB at $2,500 per month or $30,000 per annum.

Assuming the new private condominium 3 Bedroom unit is priced at $1,500,000, then the ABSD 12% is $180,000, if we divide it by $30,000, it will need 6 years rental income to recover the ABSD costs incurred.

The key important factor to consider whether to keep the HDB and pay ABSD, will be “is it worthwhile to forgo 6 years rental income to keep this HDB flat”.

Besides calculating the potential rental yield, you must also consider the potential capital appreciation, and determine the probable Return On Investment (ROI). This should then be compared to other investment options, such as bonds or equities to decide whether an additional property asset is beneficial to your investment portfolio.

You should have a strategy in place for the second property

- How long you will hold on to it (does buyer intend to sell for a profit after five years, or to hold on to it and collect rent for 30 years?)

- When and how you will cut any losses (if the property becomes a liability due to low rental income, how long will buyer hold on to property before selling it off?)

- What is your expected capital gain after holding on for 5 years. (what’s a “good price” at which you aim to sell the property?)

Most importantly, If you think about buying a new condominium while still owning a HDB flat, you may want to consider the following financial obligations.

- Fulfilling your Minimum Occupancy Period. – The law states that you are required to physically occupy your flat for Five (5) years before you can sell it on the open market. It excludes any period where you do not occupy the flat, such as when the whole flat is rented out or when there has been an infringement of the flat lease. You cannot concurrently own a HDB and buy a private property during the first 5 years of your stay in the HDB flat you’ve bought. For Singaporean, after you have purchased your new condominium, you may choose to keep your HDB, but for Singapore PR, you must dispose of your HDB flats within 6 months of buying the private property.

- Additional Buyer Stamp Duty (ABSD) – If you are a Singapore citizen, you will incur an additional buyer stamp duty of 12% on your second private property purchase. This is on top of the normal Buyer Stamp Duty of 3 or 4 %.

- Total Debt Servicing Ratio (TDSR) – From June 2013, the government introduce TDSR, to encourage home buyers to borrow within their means. It was part of the cooling measures to prevent borrowers from being over-extended with their home loans. The current rate for TDSR is at 60% of your gross monthly income. It means you cannot use more than 60% of your income to service your total loans ( that includes car loans, home loans, and credit card expenditure). So if you are buying a second private property, you have to consider how TDSR will affect your borrowing and whether you have sufficient funds if you decide not to sell your existing HDB.

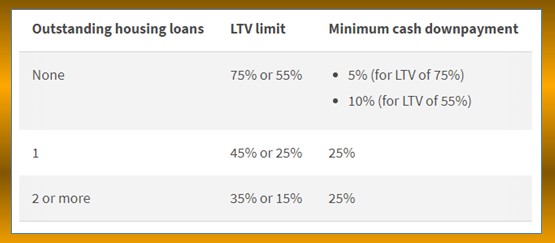

- Loan to Value (LTV) bank loans ratio – The new rules on LTV limit determines the maximum amount an individual can borrow from a financial institution (FI) for a housing loan.

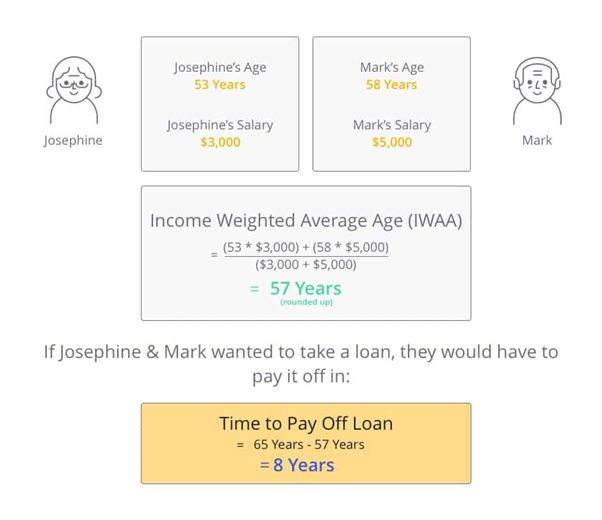

- The maximum housing loan borrowers can take depends on their age, loan duration and property type, and whether they have existing housing loans. Joint borrowers are assessed using an income-weighted average age.

- The maximum loan tenure for housing loans is capped

at:

- 30 years for HDB flats.

- 35 years for non-HDB properties.

LTV refers to the loan amount as a percentage of the property’s value. For example if the buyer borrows $750,000 to purchase a $1 million property, then LTV is 75%

As mentioned earlier, The LTV limits for individuals change depending on the number of outstanding/existing housing loans a borrower has.

Effective from 6 July 2018

We will apply the lower LTV limit (eg. 55% for None Outstanding Loan) if the loan tenure exceeds 30 years (or 25 years for HDB flats), or the loan period extends beyond the borrower’s age of 65 years.

So, bearing this in mind, the buyer has to consider his LTV if he decides to keep the existing HDB when he buys a new condominium. If the existing HDB still has outstanding loan, then his new loan will be set at LTV 45%, or he has to set aside 55% in cash & CPF to buy the new private property. And it is subjected to a max of 30 years loan tenure or cap at age 65 years old for the borrower. So, the age of the buyer must also be considered if you are to buy an additional private property.

This is because the monthly mortgage and loan tenure for the property is calculated based on age. It is either they have fewer years to pay off the loan or they will have to borrow less or pay more per month based on their age.

Example :

To summarize, if the buyer is a Singapore Citizen, and is considering owning both the existing HDB and a new private condominium, the biggest challenge to buyer is likely to come from the financial angle.

The buyer has to cater to the LTV, ABSD, and TDSR restrictions, the total amount needed to finance a second property will be a hefty sum.

With regards to use of CPF , if you buy a condo before selling your HDB , it is considered as a second property. As such you can withdraw up to a maximum of 100% of the condominium valuation limit from your CPF Ordinary Account.

And you will need to set aside your CPF Basic Retirement Sum of at least $88,000 before you can use the excess CPF money in your Ordinary Account to purchase your new condo. This is applied even if you are below 55 years old.

Therefore you will need to have plenty of hard cash on hand, it will definitely bite of a huge chunk from the savings.

Do note that property tax is payable on both properties. That is the one that you live in as well as the one that is rented out based on Annual value of the property. The tax rates range from 10 to 20% depending on the annual value of the property. So if you are renting out the condo, at $4,000/month, your property tax will be around $5,500/year.

Conclusion:

The ultimate question to ask before deciding to keep the HDB or to sell the HDB before you upgrade to a condominium is

- Can you afford to keep the HDB you own as an investment to earn rental income

- Do you need to sell the HDB flat to get funds to buy the new condo

As I have explained earlier, financial affordability is crucial and it does affect the decision. You need to have lots of hard cash, if you intend to keep your HDB.

Eg. To buy a $1.5 million private condo. You will need to have more than $1 million in cash & CPF

- LTV 45%, so you need 55% cash & CPF or $825,000

- Plus money for ABSD , another $180,000, and BSD $60,000

- Your minimum cash upfront at booking will be 25 percent

Keeping the HDB will not earn you high rental income based on current market conditions. The rental income is not enough to pay off your new mortgage amount.

It can only go towards offsetting the ABSD expenses that you have incurred.

And rental does bring along some tenancy issues and maintenance costs.

Lastly, there is another option, that is to upgrade to an executive condominium, then you will have to sell off your existing HDB under the HDB regulations. An EC will give you similar lifestyle as a condo and you must sell off your HDB thus saving you the hassle of deciding what to do.

Schedule time with meArticle contributed by Rick Fok

Rick Fok is a realtor with OrangeTee & Tie Pte Ltd. He has been in this real estate business for 9 years. He is very focus in helping his clients rent properties and he does help many customers to buy new projects according to their needs. His interest include sports such as running and soccer besides just real estate work. He loves to connect with people to discuss properties related issues and gets enormous satisfaction in helping them fulfill their needs. If you have any queries on this topic or other , please do give Rick a call and we can discuss this over a cup of coffee.

Other Articles to read

Is it better to buy an EC than a condo ?

Buying a new launch or a resale property. Which is a better property for investment?

Do you keep or sell your HDB , when you upgrade to a condominium.